What's up with all the biotech PIPEs?

An old financing tool for distressed companies is taking over the biotech world. Not because they're distressed, but because they struggle to find cash.

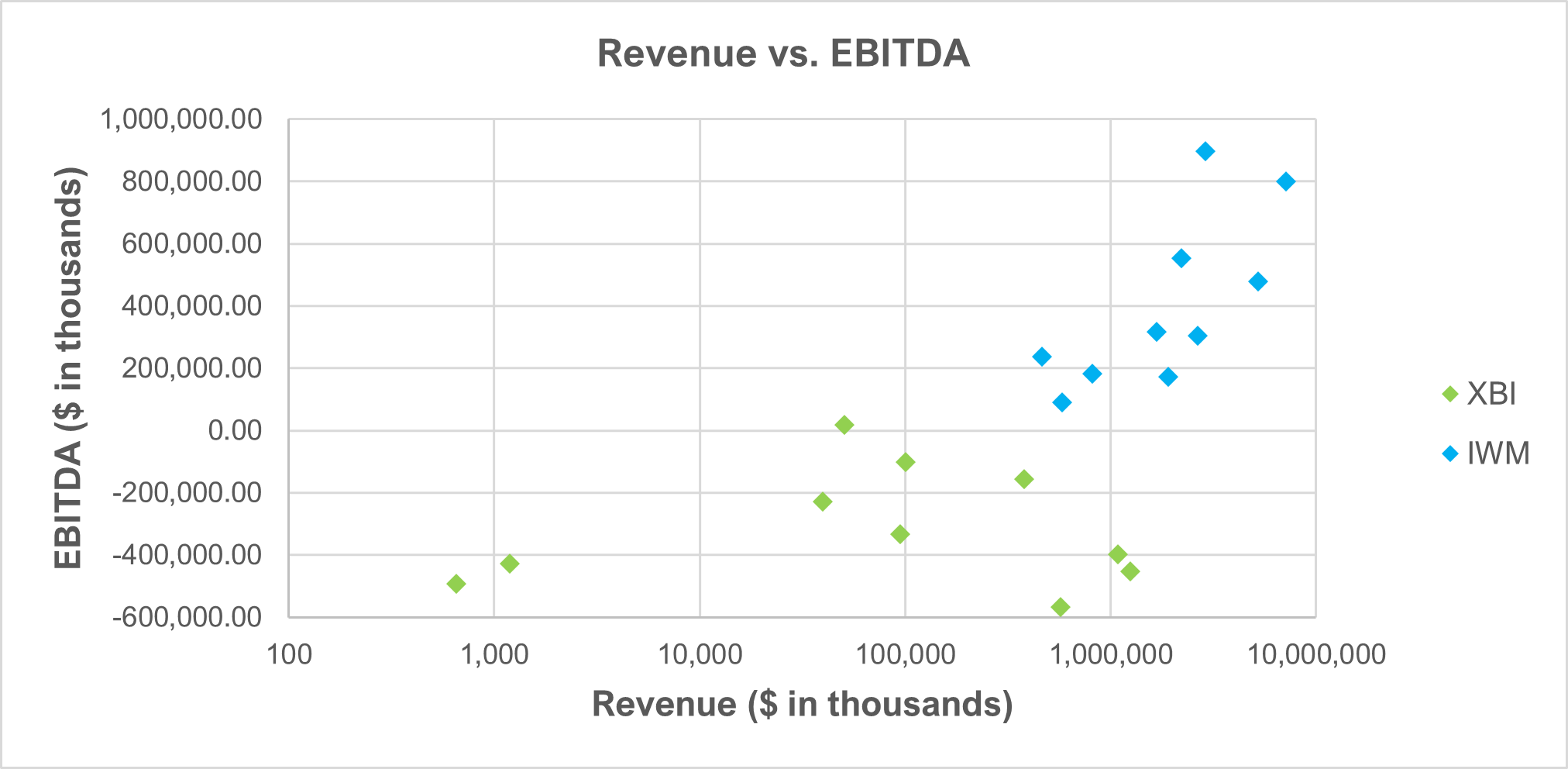

Biotech companies need cash. This does not end once they go public. A main reason is that biotechs are largely unprofitable, and the path to profitability through research & development is very capital-intensive. Indeed, the top 10 holdings of the S&P Biotech Index XBI have an average revenue of $356 million at an average EBITDA1 of negative $314 million (image above). Compare this to small-cap2 companies from the top 10 holdings of the Russell 2000 index (IWM), where we see an average revenue of $2.5 billion at an average EBITDA of $403 million. There is no need to calculate margins when the operator is different: early-stage biotech companies struggle to be profitable.

When companies need cash but do not generate sufficient profits, they have two basic ways of obtaining it:

They can issue debt, requiring them to repay it with interest over time.

They can issue more equity, giving up additional ownership of the company and its future cash flows.

Biotechs have the somewhat unique problem that many of their assets are intangible (e.g. patents). This makes access to bank loans very difficult. Most of them also don’t have access to public debt markets as they do not have a long-term credit rating3. Hence, issuing debt is almost impossible. Indeed, if we look at the debt-to-equity ratio of three biotech companies (Denali, Avidity, Kura; image below), none of these carries more than 5% debt compared to their equity. Large companies, on the other hand, often choose leverage so as not to give up much ownership. The S&P 500 average is around 1.5. Companies in that size range have the benefit of choice: A large pharmaceutical company such as Lilly can choose to be around 1.7, and a company with astronomical cash flows such as NVIDIA can afford to be around 0.22.

Unable to grow via debt, biotech companies hence need to issue equity in order to obtain cash. This is not new. In recent months, however, there is a growing trend of how they go about issuing equity. Let’s take a look at the three companies mentioned above:

On February 29th, Avidity Biosciences announced an oversubscribed $400 million financing round led by nine investors including RA Capital and Farallon.

On February 27th, Denali Therapeutics announced a $500 million financing round from unnamed health care-focused investors.

On January 26th, Kura Oncology announced an oversubscribed $150 million financing round led by previous investors such as EcoR1 Capital.

These are just three recent examples of a wave of private investments into public equity, or PIPEs, in biotech. Adam Feuerstein over at STAT News reports counting 30 such deals this year, and the Wall Street Journal reported 56 PIPEs in 2023 totaling over $4.5 billion. PIPEs are hot right now, and debates around the nature of biotech PIPE transactions among stakeholders have begun. Here, we will take a look at why PIPE deals are becoming so prevalent, what “insider trading” has to do with all of this, and what the future holds for this controversial type of funding.

Why PIPEs are so popular right now

PIPEs are used by companies to raise cash as somewhat of an alternative to the more classical registered secondary offering. Instead of offering new shares to the public, the company offers them to accredited investors, typically at a discount to the current share price. Historically, PIPEs were popular as a form of quick financing for distressed companies. Warren Buffett famously injected $5 billion into Goldman Sachs to save the bank from bankruptcy in 2008. Especially in recent years, however, PIPEs have become popular as a form of growth capital for companies.

PIPEs have a couple of advantages compared to public secondary offerings. They do not require as many regulatory disclosures as a registered secondary offering, making them generally faster and more easily accessible. Given their private nature, they also offer some more flexibility and privacy to negotiate transaction terms with investors.

It is these transaction negotiations that have caused debates around PIPEs. Due to the fact that PIPEs in biotech almost always involve the disclosure of material, non-public information (MNPI) such as clinical trial results, I have heard them be referred to as a form of “legal insider trading” a lot recently. So, let’s take a look at these accusations.

Isn’t this insider trading?

PIPE deals are subject to certain forms of regulation which are supposed to secure existing shareholders. For instance, the shares sold in the PIPE transaction cannot be traded before they are registered with the SEC, which typically happens within the first two months of disclosure to the public4. If MNPI such as clinical trial results have been disclosed, shares are untradable until that information is made publicly available. This is, in short, why the disclosure and the obtaining of shares do not constitute insider trading.

Many, however, do not agree. Adam Feuerstein from STAT News notes that “The sharing of material, non-public information is a big reason why PIPEs are so hot right now.” If the main reason for the investment is the obtained insider information (and profiting from it), it is easy to see why people would be upset. But, what if the root cause for these deals is not in the insider information? Let’s change perspective for a second and look at PIPE deals from the side of biotech companies. Why do they choose to obtain funding via PIPEs?

The Biotech Side

Companies seek for investors in PIPEs, not the other way around. The reason for PIPEs gaining popularity hence needs to have something to do with the biotech companies.

Biotech has been through a rough patch. Over the last five years, the earlier mentioned biotech index ETF XBI is at a cumulative annual growth rate of 6.8% and is still trading at 36% below February 2021 highs (image below). A $10,000 investment into the S&P500 would have returned $22,165 by now, whereas the same investment into XBI would have returned $13,753. Even other capital-intensive industries such as Metals & Mining returned almost three times the annual growth rate of XBI.

It is unsurprising, then, that investor confidence hit rock-bottom at some point last year. In capital markets, less confidence equals higher risk assumptions, and higher risk assumptions equal a greater cost of equity, or the returns that investors require for an investment to be considered “worth it”.

As we discussed, biotech companies need to issue equity as they are very limited in their ability to issue debt. If they were to issue equity via a registered secondary offering, in the current climate of market confidence, the offering would likely have to be at a hefty discount.

Another factor we cannot ignore are interest rates. Returns from unprofitable companies are much more sensitive to interest rates, as this article in the Wall Street Journal points out. Interest rates surged last year and appear to remain high-for-longer. This adds to the risk assumptions in secondary offerings, which would in turn drive the necessary discount even higher.

In a PIPE, on the other hand, you don’t work with the broader market. You work with accredited investors to whom you can show why their investment will pay off, and this is where MNPI disclosure comes in handy. Positive clinical trial results will increase investor confidence and might hence allow biotechs to offer shares at less of a discount than they would have to give to the public market, especially if the investors have experience in the industry.

So, PIPEs give companies that have gone out-of-favor with the market due to low performance and high interest rates an opportunity to raise cash faster and cheaper than in registered secondary offerings. The disclosure of MNPI undeniably plays a part in this, but it is not the only reason companies are choosing this form of financing.

Let us also take a moment to consider the alternative: what happens if sharing MNPI in PIPEs was not allowed?

Secondary offerings will be limited to companies in very attractive fields (e.g. weight loss drugs) and to companies who are willing to offer higher discounts. This will be a limited pool of companies. Some companies might choose to delay expansion projects, others might choose more conservative over riskier projects. One has to wonder if all of this would be in the interest of existing shareholders. Surely, a public secondary offering based on public information would be “more fair”. But if it comes at the potential cost of existing shareholders, and possibly at the cost of innovation, are we going to have a net positive effect on the industry and the market?

What’s next?

The cost of equity for biotech companies is sky-high, and as long as interest rates remain elevated and investor confidence is recovering, this will not change. PIPEs are a tool that the companies use to deal with this climate. Based on recent trends, I think PIPEs in biotech are here to stay, but I wouldn’t expect there to be continued increases as we have seen in the last year once the Federal Reserve cuts interest rates. When investor confidence in the general investor public picks back up, there might even be a decrease in PIPEs. Take Viking Therapeutics, for instance, who raised funds via a public offering after the positive Phase II trial results on their weight loss drug VK2735 sent the stock flying.

A lot of the public discourse on PIPEs will likely also depend on how companies manage the disclosures. Avidity, for instance, announced the PIPE deal on Thursday, February 29th. On Friday, the stock surged by 20%. On March 4th, before market opening, the company announced the trial results. Granted, not all PIPE transactions are handled this way, but timely disclosures of the trial results upon closing the PIPE deal is important.

I am curious how the debate will continue, and if we will see regulatory changes. For now, it looks to me as if these PIPEs are a net positive for the industry and common shareholders.

If you’re new to EBITDA, here is a good introductory article. EBITDA: Definition, Calculation Formulas, History, and Criticisms (investopedia.com). In short, it is a quick measure of cash profitability.

Small-cap companies are broadly defined as companies with a market capitalization of up to $2 billion. Most public biotech companies are small-caps.

And, if they had one, it would be very bad.

As the PIPE deal itself is non-public until disclosure, investors are also not allowed to trade shares before the shares are registered with the SEC. In a famous case back in 2007, hedge fund managers shorted stock of a company that they invested in and then used the PIPE shares to cover their short position.